Middle East conflict: The impact on UK travel

Middle East conflict: The impact on UK travel

Emily Williams

Research Executive

Damaged confidence, heightened safety concerns, and the possibility of increased travel costs are just a few trends that have emerged in the first months following the outbreak of conflict in the Middle East. Yet despite this, and the uncertainty faced by consumers already grappling with the cost-of-living crisis, data sources indicate that travel demand remains resilient. UK holidaymakers are continuing to plan trips, but are adapting by reconsidering their destinations, how they book, and redefining what they perceive as ‘safe’.

Damaged confidence, heightened safety concerns, and the possibility of increased travel costs are just a few trends that have emerged in the first months following the outbreak of conflict in the Middle East. Yet despite this, and the uncertainty faced by consumers already grappling with the cost-of-living crisis, data sources indicate that travel demand remains resilient. UK holidaymakers are continuing to plan trips, but are adapting by reconsidering their destinations, how they book, and redefining what they perceive as ‘safe’.

Damaged confidence, heightened safety concerns, and the possibility of increased travel costs are just a few trends that have emerged in the first months following the outbreak of conflict in the Middle East. Yet despite this, and the uncertainty faced by consumers already grappling with the cost-of-living crisis, data sources indicate that travel demand remains resilient. UK holidaymakers are continuing to plan trips, but are adapting by reconsidering their destinations, how they book, and redefining what they perceive as ‘safe’.

Initial response: uncertainty and delayed booking patterns

The immediate impact of the conflict was operational disruption: flight cancellations, rerouting, longer journey times and constrained capacity. Given the Gulf's role as a key transit route to Asia, Australasia, and parts of Africa, these disruptions led to longer journeys, higher costs, and fewer convenient options. While those who had booked trips to the Middle East and surrounding countries rushed to cancel, those still in the planning stage chose to respond by delaying, triggering a ‘window shopping gap’.

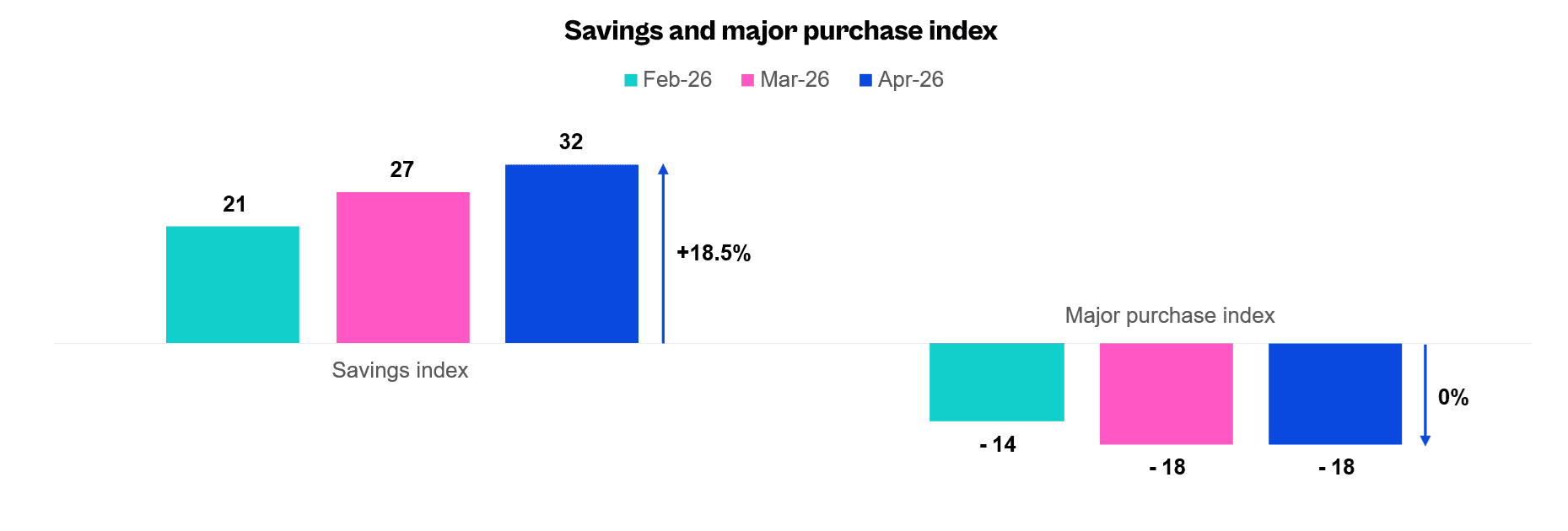

Consumer confidence has dropped by 6 points to -25 since the conflict began, the largest decline in a year and the lowest level since 2023. According to GfK data, the decline in significant expenditure on items such as holidays has led individuals to save their money instead, reflecting a cautious, ‘wait and see’ approach to spending decisions. Additionally, the inflation rate has increased by 0.3% since the conflict began, yet consumer intention to book a holiday remained flat year-on-year. People still want to take trips; they’re just doing so with care.

That said, this ‘watching and waiting’ phase did result in travel spend falling by 3.3% year-on-year, according to Barclaycard, the first decline since pandemic-related travel restrictions. Cost concerns continue to weigh heavily, with seven in ten people saying they will cut back on travel, and nearly three-quarters (74%) expecting ongoing regional tensions to further affect the cost of living throughout the remainder of the year.

The immediate impact of the conflict was operational disruption: flight cancellations, rerouting, longer journey times and constrained capacity. Given the Gulf's role as a key transit route to Asia, Australasia, and parts of Africa, these disruptions led to longer journeys, higher costs, and fewer convenient options. While those who had booked trips to the Middle East and surrounding countries rushed to cancel, those still in the planning stage chose to respond by delaying, triggering a ‘window shopping gap’.

Consumer confidence has dropped by 6 points to -25 since the conflict began, the largest decline in a year and the lowest level since 2023. According to GfK data, the decline in significant expenditure on items such as holidays has led individuals to save their money instead, reflecting a cautious, ‘wait and see’ approach to spending decisions. Additionally, the inflation rate has increased by 0.3% since the conflict began, yet consumer intention to book a holiday remained flat year-on-year. People still want to take trips; they’re just doing so with care.

That said, this ‘watching and waiting’ phase did result in travel spend falling by 3.3% year-on-year, according to Barclaycard, the first decline since pandemic-related travel restrictions. Cost concerns continue to weigh heavily, with seven in ten people saying they will cut back on travel, and nearly three-quarters (74%) expecting ongoing regional tensions to further affect the cost of living throughout the remainder of the year.

The immediate impact of the conflict was operational disruption: flight cancellations, rerouting, longer journey times and constrained capacity. Given the Gulf's role as a key transit route to Asia, Australasia, and parts of Africa, these disruptions led to longer journeys, higher costs, and fewer convenient options. While those who had booked trips to the Middle East and surrounding countries rushed to cancel, those still in the planning stage chose to respond by delaying, triggering a ‘window shopping gap’.

Consumer confidence has dropped by 6 points to -25 since the conflict began, the largest decline in a year and the lowest level since 2023. According to GfK data, the decline in significant expenditure on items such as holidays has led individuals to save their money instead, reflecting a cautious, ‘wait and see’ approach to spending decisions. Additionally, the inflation rate has increased by 0.3% since the conflict began, yet consumer intention to book a holiday remained flat year-on-year. People still want to take trips; they’re just doing so with care.

That said, this ‘watching and waiting’ phase did result in travel spend falling by 3.3% year-on-year, according to Barclaycard, the first decline since pandemic-related travel restrictions. Cost concerns continue to weigh heavily, with seven in ten people saying they will cut back on travel, and nearly three-quarters (74%) expecting ongoing regional tensions to further affect the cost of living throughout the remainder of the year.

The shift in destination demand

Where the impact becomes unmistakable is in destination choice. Even for people who are venturing to countries far from areas of conflict, the perceived safety of a destination and a heightened sense of instability have influenced their decision-making.

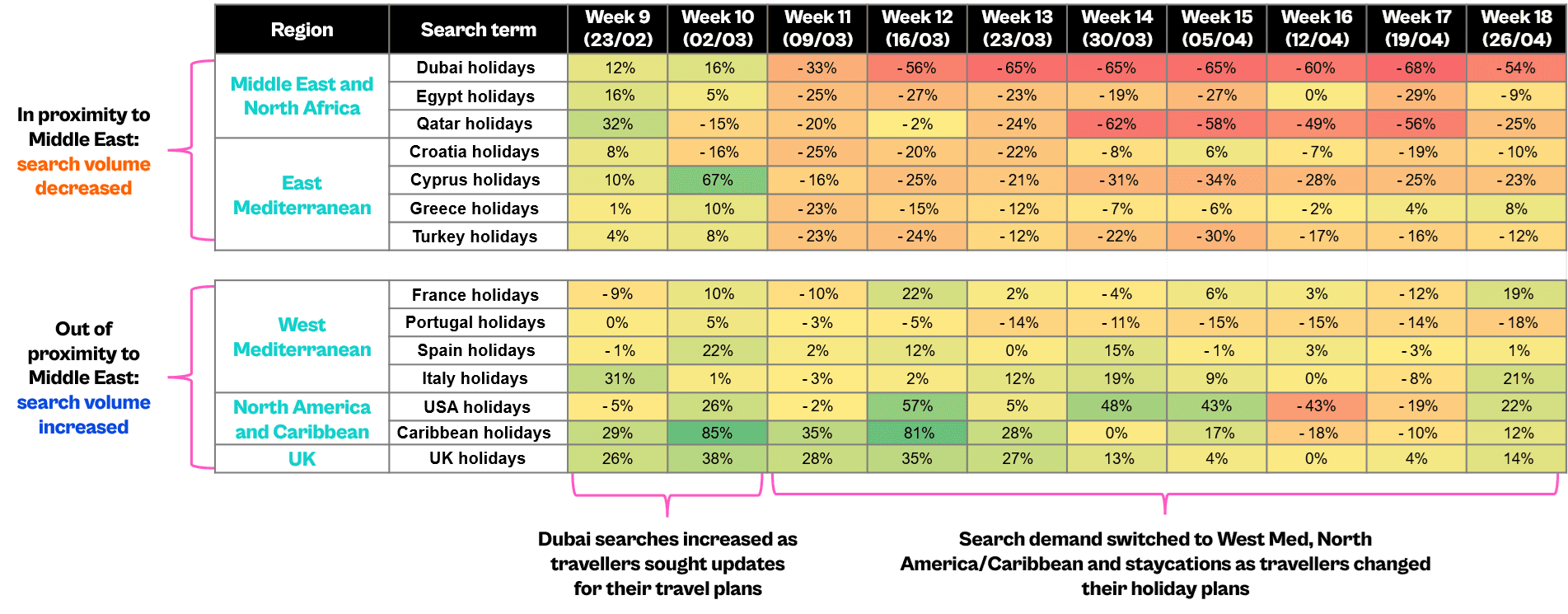

A couple of weeks after the outbreak of the war, Google search interest dropped sharply for the Middle East (-33% Dubai), North Africa (-25% Egypt), and surrounding countries (-23% Turkey), while the West saw an uplift. UK travellers are instead searching for holidays in distant destinations far from the conflict zone, such as the Caribbean, or sticking to familiar places in Europe and the UK. Domestic holidays have seen a 28% average increase in Google search data, and traffic to domestic travel websites has outpaced overseas categories month-on-month.

According to a recent Google report, the shift towards staycations and short-haul holidays is further underscored by an increase in ad clicks for domestic and nearby European destinations, as well as a 1.2% rise in spending on UK-based hotels and accommodation. Rather than completely giving up their plans, people are shifting their attention elsewhere.

Where the impact becomes unmistakable is in destination choice. Even for people who are venturing to countries far from areas of conflict, the perceived safety of a destination and a heightened sense of instability have influenced their decision-making.

A couple of weeks after the outbreak of the war, Google search interest dropped sharply for the Middle East (-33% Dubai), North Africa (-25% Egypt), and surrounding countries (-23% Turkey), while the West saw an uplift. UK travellers are instead searching for holidays in distant destinations far from the conflict zone, such as the Caribbean, or sticking to familiar places in Europe and the UK. Domestic holidays have seen a 28% average increase in Google search data, and traffic to domestic travel websites has outpaced overseas categories month-on-month.

According to a recent Google report, the shift towards staycations and short-haul holidays is further underscored by an increase in ad clicks for domestic and nearby European destinations, as well as a 1.2% rise in spending on UK-based hotels and accommodation. Rather than completely giving up their plans, people are shifting their attention elsewhere.

Where the impact becomes unmistakable is in destination choice. Even for people who are venturing to countries far from areas of conflict, the perceived safety of a destination and a heightened sense of instability have influenced their decision-making.

A couple of weeks after the outbreak of the war, Google search interest dropped sharply for the Middle East (-33% Dubai), North Africa (-25% Egypt), and surrounding countries (-23% Turkey), while the West saw an uplift. UK travellers are instead searching for holidays in distant destinations far from the conflict zone, such as the Caribbean, or sticking to familiar places in Europe and the UK. Domestic holidays have seen a 28% average increase in Google search data, and traffic to domestic travel websites has outpaced overseas categories month-on-month.

According to a recent Google report, the shift towards staycations and short-haul holidays is further underscored by an increase in ad clicks for domestic and nearby European destinations, as well as a 1.2% rise in spending on UK-based hotels and accommodation. Rather than completely giving up their plans, people are shifting their attention elsewhere.

Protection, flexibility and trust became decisive

Travellers are not only seeking reassurance when choosing where to go, but also in how they arrange their holidays. Holidaymakers are increasingly seeking financial protection and flexible booking choices to safeguard against uncertainty. Google data shows that branded searches decreased by 7.1%, indicating a rise in discovery-driven queries, which reflects a more deliberate and informed approach to planning. The growing need for security is also evident in the heightened interest in travel insurance. Searches by European travellers have risen 32% year-on-year, as many look for extra coverage against cancellations and disruptions.

One-third of travellers now say that global events are shaping their travel decisions, and 46% now place greater importance on flexibility and guarantees. The percentage of people concerned about rising travel expenses has jumped from 59% to 70%, while worries about travel disruptions have also increased modestly. These anxieties have led to a year-on-year drop in spending at travel agents (-4.6%), airlines (-4.1%), and public transportation (-2.9%).

Travellers are not only seeking reassurance when choosing where to go, but also in how they arrange their holidays. Holidaymakers are increasingly seeking financial protection and flexible booking choices to safeguard against uncertainty. Google data shows that branded searches decreased by 7.1%, indicating a rise in discovery-driven queries, which reflects a more deliberate and informed approach to planning. The growing need for security is also evident in the heightened interest in travel insurance. Searches by European travellers have risen 32% year-on-year, as many look for extra coverage against cancellations and disruptions.

One-third of travellers now say that global events are shaping their travel decisions, and 46% now place greater importance on flexibility and guarantees. The percentage of people concerned about rising travel expenses has jumped from 59% to 70%, while worries about travel disruptions have also increased modestly. These anxieties have led to a year-on-year drop in spending at travel agents (-4.6%), airlines (-4.1%), and public transportation (-2.9%).

Travellers are not only seeking reassurance when choosing where to go, but also in how they arrange their holidays. Holidaymakers are increasingly seeking financial protection and flexible booking choices to safeguard against uncertainty. Google data shows that branded searches decreased by 7.1%, indicating a rise in discovery-driven queries, which reflects a more deliberate and informed approach to planning. The growing need for security is also evident in the heightened interest in travel insurance. Searches by European travellers have risen 32% year-on-year, as many look for extra coverage against cancellations and disruptions.

One-third of travellers now say that global events are shaping their travel decisions, and 46% now place greater importance on flexibility and guarantees. The percentage of people concerned about rising travel expenses has jumped from 59% to 70%, while worries about travel disruptions have also increased modestly. These anxieties have led to a year-on-year drop in spending at travel agents (-4.6%), airlines (-4.1%), and public transportation (-2.9%).

Accord’s perspective

Travel was the top category for increased UK consumer spending in January 2026, with search activity rising in both January and February. However, amid geopolitical tensions and rising living costs, we have seen a knock-on effect on consumer confidence and search demand across specific regions, halting the growing momentum.

Although the Bank of England decided to keep the interest rate at 3.75% in April, some analysts believe rate rises are on the cards later this year. Unstable oil prices, incidents like those in the Strait of Hormuz, and news of jet fuel shortages leading to flight cancellations all threaten traveller confidence and drive up costs.

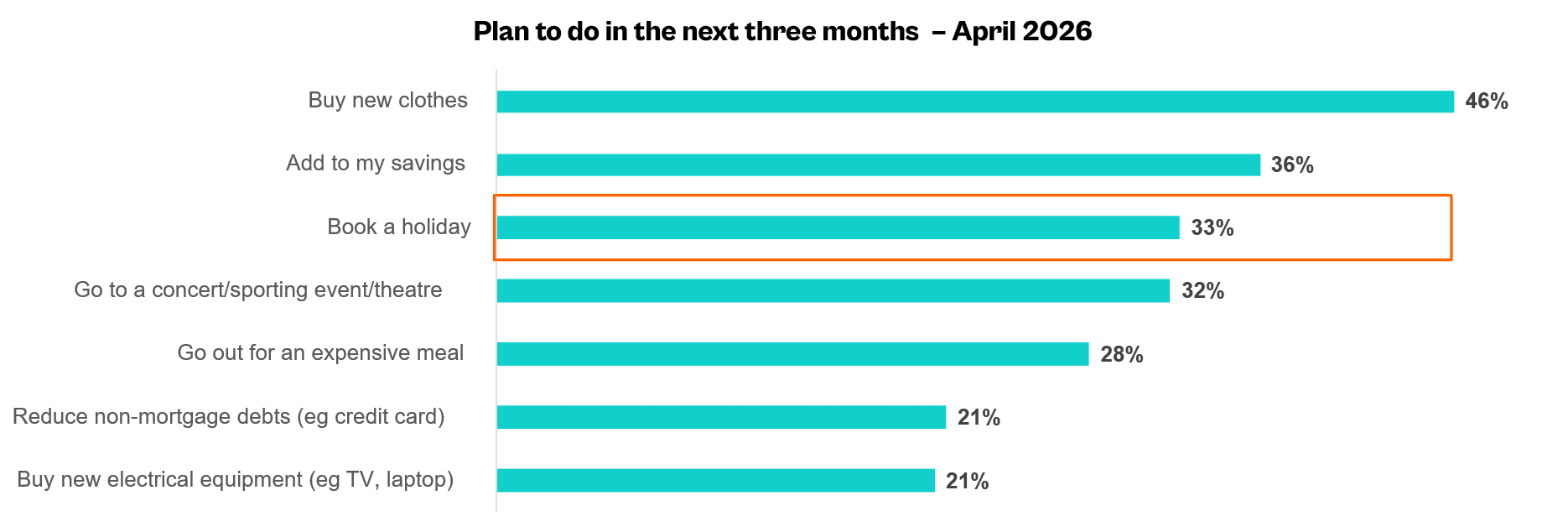

Yet British travellers have proven remarkably resilient. Travel's status as the 'most essential non-essential' holds firm: as the Mintel data below shows, people continue to prioritise holidays, even under financial pressure. What we're seeing is a shift in where people want to go, not whether they want to go at all.

As consumer confidence begins to recover, brands that prioritise transparency, flexibility and robust customer protections will be best positioned to turn renewed interest into confirmed bookings. By giving travellers greater reassurance and control throughout the booking journey, these companies will build trust, strengthen loyalty and convert demand more effectively in an increasingly competitive market.

Travel was the top category for increased UK consumer spending in January 2026, with search activity rising in both January and February. However, amid geopolitical tensions and rising living costs, we have seen a knock-on effect on consumer confidence and search demand across specific regions, halting the growing momentum.

Although the Bank of England decided to keep the interest rate at 3.75% in April, some analysts believe rate rises are on the cards later this year. Unstable oil prices, incidents like those in the Strait of Hormuz, and news of jet fuel shortages leading to flight cancellations all threaten traveller confidence and drive up costs.

Yet British travellers have proven remarkably resilient. Travel's status as the 'most essential non-essential' holds firm: as the Mintel data below shows, people continue to prioritise holidays, even under financial pressure. What we're seeing is a shift in where people want to go, not whether they want to go at all.

As consumer confidence begins to recover, brands that prioritise transparency, flexibility and robust customer protections will be best positioned to turn renewed interest into confirmed bookings. By giving travellers greater reassurance and control throughout the booking journey, these companies will build trust, strengthen loyalty and convert demand more effectively in an increasingly competitive market.

Travel was the top category for increased UK consumer spending in January 2026, with search activity rising in both January and February. However, amid geopolitical tensions and rising living costs, we have seen a knock-on effect on consumer confidence and search demand across specific regions, halting the growing momentum.

Although the Bank of England decided to keep the interest rate at 3.75% in April, some analysts believe rate rises are on the cards later this year. Unstable oil prices, incidents like those in the Strait of Hormuz, and news of jet fuel shortages leading to flight cancellations all threaten traveller confidence and drive up costs.

Yet British travellers have proven remarkably resilient. Travel's status as the 'most essential non-essential' holds firm: as the Mintel data below shows, people continue to prioritise holidays, even under financial pressure. What we're seeing is a shift in where people want to go, not whether they want to go at all.

As consumer confidence begins to recover, brands that prioritise transparency, flexibility and robust customer protections will be best positioned to turn renewed interest into confirmed bookings. By giving travellers greater reassurance and control throughout the booking journey, these companies will build trust, strengthen loyalty and convert demand more effectively in an increasingly competitive market.

" transform="translate(0 20)" width="997px"/></svg>)

Read more

Discuss your next project with us...

To learn more about what we can offer and how we can work together, we’d love to hear from you.

London

Accord Marketing,

1 Waterhouse Square, London EC1N 2ST.

South-West

The Node, 1 Enterprise Road,

Roundswell, Barnstaple,

Devon EX31 3YB.

All enquiries

02072 712 481

Assume nothing.

Discuss your next project with us...

To learn more about what we can offer and how we can work together, we’d love to hear from you.

London

Accord Marketing,

1 Waterhouse Square, London EC1N 2ST.

South-West

The Node, 1 Enterprise Road,

Roundswell, Barnstaple,

Devon EX31 3YB.

All enquiries

Discuss your next project with us...

To learn more about what we can offer and how we can work together, we’d love to hear from you.

London

Accord Marketing,

1 Waterhouse Square, London EC1N 2ST

South-West

The Node, 1 Enterprise Road,

Roundswell Barnstaple,

Devon EX31 3YB

All enquiries

020 72712481